|

Spiraling polymer prices are causing great concerns to plastics

processors as well user and allied industries, and have been the

hot topic of discussions over the last few months. Escalating oil

prices have been blamed for the rise in feedstock prices, which

in turn have led to rising polymer prices, currently lingering at

record peak levels. When will the rise in oil prices and subsequently

feedstock prices be arrested? When will polymer prices stabilise

and at what levels? Will the worldwide economies after a sluggish

2002-2003, face obstacles in the path to recovery? Will polymer

demand be affected by high prices? These are few of the questions

raised by our readers. In this feature, we attempt to answer many

of them thus:

|

When did polymer prices start rising? |

|

Global Oil Scenario |

|

Factors affecting Polymer prices

The basic prices of oil, ethane, propane, gas

and naphtha

Capacity utilization

Demand-supply balance

|

|

When will polymer prices stabilize? |

When did polymer prices start rising?

When did polymer prices start rising?

As per industry, rising oil prices lead to a rise in feedstock prices,

creating a mothball effect on polymer prices. Hence, oil price hikes

should preceed polymer price hikes.

As represented in the following graphs, oil prices remained fairly

stable over a long period from January 2003 until April 2004. However,

feedstock prices started rising, particularly in Q1-2004; increasing

by 10% or more. This increase in polymer prices could be ascribed

mainly to overall increase in their demand.

In a reversal of trend, while oil prices rose by 10% in Q2-2004,

polymer price hikes did not match the pace and slowed down.

Interestingly polymer price increase

continued during Q2-2004, albeit somewhat slowly, despite an increase

in oil prices by 10% in the same period. Prices of all polymers

went up significantly from the beginning of Q3-2004.

Very minimum correlation between the increase in the price of oil,

naphtha and other feedstock and the increase in the prices of polymers

can be seen in this period.

Let us look at the increase in the prices of oil, feedstocks and

polymers and ascertain whether an increase in oil prices has resulted

in the increase in prices of the basic feedstocks or is booming

demand leading to an increase in polymer prices?

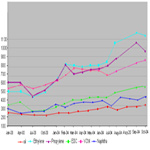

Movement of Oil, Naphtha, EDC, VCM, Ethylene, Propylene from Jan

03-Oct 04

Movement of Oil, Naphtha, EDC, VCM, Ethylene, Propylene from Jan

03-Oct 04

Movement of Oil, Naphtha, Ethylene, Propylene, Polyethylenes from

Jan 03-Oct 04

Movement of Oil, Naphtha, Ethylene, Propylene, Polyethylenes from

Jan 03-Oct 04

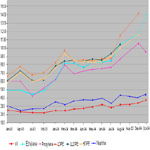

Movement of Oil, Naphtha, Propylene, Ethylene, Polypropylene from

Jan 03-Oct 04

Movement of Oil, Naphtha, Propylene, Ethylene, Polypropylene from

Jan 03-Oct 04

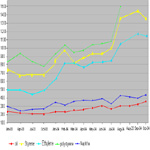

Movement of Oil, Naphtha, Ethylene, Styrene, Polystyrene from Jan

03-Oct 04

Movement of Oil, Naphtha, Ethylene, Styrene, Polystyrene from Jan

03-Oct 04

Global Oil Scenario

Oil prices remained stable around US$32/barrel in early 2004, but

shot up beyond US$45/barrel around mid August and peaked at approx

US$50 end of September. Interestingly the gap between Middle East

price and Brent has widened to almost US$ 8-10/barrel indicating

speculative trading. (While Brent price is at US$50/barrel, Dubai

price is only around US$41/barrel). The flaring of oil price despite

an increase in the oil production by OPEC countries seems unjustified.

However, the global demand of oil, and that too from Asia and USA

has increased significantly. China alone has imported 40% more oil

this year so far. If the increase in the oil price continues for

a longer period, it could fuel inflation in 2005, adversely impacting

economy all around. However, IMF and World Bank still opine that

oil prices would remain on the higher side, yet would not dampen

the overall demand. The turbulence in oil prices during the last

3 months has been caused by some of the following factors:

|

Increase in energy demand |

|

Disruption in supply from Iraq, Nigeria, Russia and Venezuela |

|

Limited possibility of an increased supply from the OPEC region |

To read in detail, click here : Why

are oil prices rising?

Polymer prices depend upon

|

The basic prices of oil, ethane, propane, gas and naphtha. |

|

Capacity utilization |

|

Demand-supply balance |

The basic prices of oil, ethane, propane, gas and naphtha :

Global feedstock share for Ethylene production is Naphtha (53%),

Ethane (30%) and other feedstocks like propane, butane, gas oil

(17%). In the Asia Pacific region almost 80% of the Ethylene capacity

is based on Naphtha; whereas, in the Middle East almost 70% ethylene

capacity is based on Ethane. The cost of producing ethylene from

ethane in the USA is 3-4 times more than in the Middle East, but

the difference in the cost between the 2 regions for producing ethylene

from naphtha is hardly around 25%.

The petrochem plants depending on ethane, propane, gas and naphtha

as feedstock and subsequently ethylene and propylene face obstacles

in the form of a supply crunch as well as prevalent high prices.

However, very minimum correlation between the increase in the price

of oil, naphtha and other feedstock and the increase in the prices

of polymers can be seen in this period. Maximum price increase is

seen in Polystyrene and the least in PVC, possibly since Polystyrene

has to depend upon Ethylene and Benzene - both derived from oil,

while PVC depends only partly for feedstock inputs from oil.

Capacity utilization

The petrochemicals cycle peaks every 7 years. This is largely due

to the fact that as product prices increase, the manufacturers go

ahead with capacity addition. Once the capacity becomes operational

and supply outstrips demand, producers feel the pressure on margins

as competition does not allow increase in prices. As a result, prices

decline and this continues until there is further recovery in economic

performance. However, at the time of this petrochem peak, there

has been no such significant capacity expansion resulting in a tight

supply situation. The pressure of growing demand has aided in increasing

capacity utilization of polymer plants during the last couple of

years, expected to come down only when more capacity will start

going onstream towards end of 2005. Almost 13 million tons of only

Polyethylene capacity is expected to be installed and on stream

globally between 2005 and 2008, of which over 70% will be in the

Middle East and Asia-Pacific region.

Demand Supply Balance

Meanwhile, global economies are recovering all over, showing signs

of a positive change since the last two quarters of 2003. To read

GDP growth forecasts amid soaring oil prices

click here

Growing economies will definitely exert pressures

on the overall demand for polymers, directly or indirectly since

plastics are the major input/raw material for major growth drivers

of the economy: sectors such as housing and construction,

FMCG, packaging, automotive, etc. As for the domestic markets, infrastructure projects such

as telecom, road development and construction coupled with government

policies favouring agriculture and rural construction has buoyed

the markets for petrochemicals. The demand for polymers has seen

an increase of about 4% in 2003. The global economy seems to be

heating up, putting pressure on polymer demand. However, supply

side will gear up only in 2006, leading to a situation of demand-supply

imbalance expected to ease only when more capacity will go on stream.

Estimates of demand-supply indicate that pressures on supply may

ease after 2006.

When will polymer prices stabilize?

The impact of higher capacity will only be felt after 2006.

Until then polymer prices are expected to remain higher because

the overall demand of polymers is expected to be higher on account

of an overall improved economy. The global economy is expected to

show a healthy growth of about 4-5% in 2004 and most likely in 2005.

The fear of terrorism is likely to be seized after the US Presidential

election. Oil supply is expected to be more stable in 2005. It would

therefore not be surprising if oil prices get stabilized at lower

range of US$35-40/barrel. This will eventually have a positive impact

on the prices of polymers. Further, in the global scenario, factors

such as rising interest rates and slowing down in the Chinese demand

could possibly affect the uptrend.

Most pundits believe that the polymer prices will reduce at least

by 15% from the existing level by early 2005. Polymer demand will

be buoyant at least until 2006 when newer capacity will be commissioned.

The plastic processors need not panic due to higher prices of raw

material because the future holds bright for them at least until 2006.

|